New Research Reveals the Consumer Goods Battle for B2B and B2C Relationships

The B2B relationship between CG companies and traditional retailers still drives the vast majority of CG sales, so solving problems in this relationship will be key to success.

Heike Young

For both consumers and consumer goods (CG) companies, the traditional landscape of physical shelf space and shopping carts will never be the same. Today’s consumers have total control of where and how they buy — plus unprecedented access to product and fulfillment options.

To remain relevant, competitive, and future-proof, CG brands are optimizing operations, from product development to distribution. In a recent survey of 500 global CG leaders, we examined the state of consumer goods, uncovering:

- Why digital transformation is an urgent imperative

- What leaders must do to build more effective business-to-business (B2B) and business-to-consumer (B2C) relationships

- How leaders can evolve for the future

We compiled our findings in Consumer Goods and the Battle for B2B and B2C Relationships. Here’s a preview of key findings from the report.

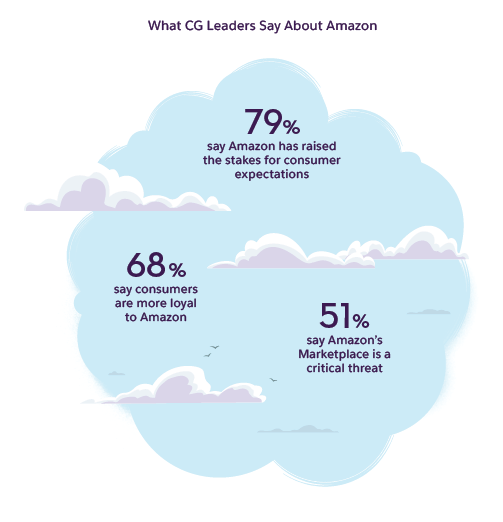

CG leaders have concerns about Amazon and changing consumer behaviors

You can’t talk about retail and CG transformation without noting the elephant in the room: Amazon. A vast majority of CG leaders (79%) say Amazon has raised the stakes for consumer expectations. Sixty-eight percent think that consumers are more loyal to Amazon’s marketplace than individual brands.

These concerns aren’t unfounded. One recent consumer study shows that while 50% of consumers make a first-time product purchase directly from a retailer and 31% buy from marketplaces like Amazon, their second purchase is a different story: 47% of consumers choose marketplaces for that second purchase vs. only 34% returning to retailers.

To stay competitive, CG companies must look beyond the traditional supply chain and product development models. That means leading with experience (think personalized Coca-Cola cans or Kiehl’s custom skincare formulas) and seamless distribution.

Poor in-store execution costs CG companies big money

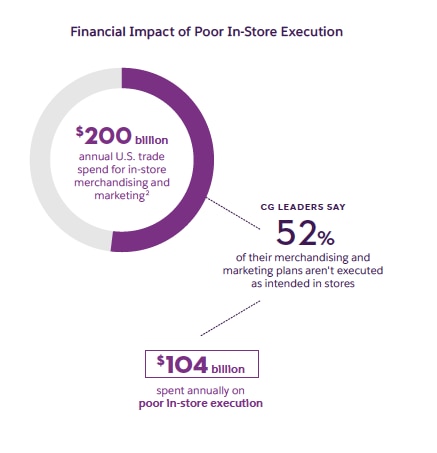

Fast-moving consumer goods revenue is $1.01 trillion annually in the U.S. — and 95% of those sales still come from traditional brick-and-mortar retail. However, when asked what percentage of their merchandising and marketing plans are executed as intended at brick-and-mortar retail locations, CG leaders said only 48% hit the mark. At the same time, CG leaders in the U.S. spend $200 billion annually on trade spend for merchandising and marketing.

That means CG companies are putting $104 billion of spending in the U.S. at risk due to poor in-store execution. Poor relationships between CG companies and traditional retailers come with a high price tag. Consumers expect their favorite products to be available at the right price at the right time, and when retail execution is sub-par, so is consumer experience.

CG leaders are challenged to build effective B2B relationships

When it comes to their relationship with retailers, CG leaders are keeping an eye on burgeoning private-label lines that compete against their own products.

Forty-nine percent of leaders perceive retailers’ private label products as a business threat, as powerful private-label brands from the likes of Tesco, Hema, Costco, Amazon, and Walmart soar. In 2018, Costco’s Kirkland brand earned nearly $40 billion — an 11% increase from 2017 (and more sales than Campbell Soup, Kellogg’s, and Hershey combined).

In an industry where access to end-consumer data is integral to accelerating innovation and time to market, less than half (43%) of CG leaders are completely satisfied with their ability to leverage customer insights from retailers. That’s unfortunate because data is the bedrock of AI efforts that can build personalization, convenience, and automation capabilities.

The B2B relationship between CG companies and traditional retailers still drives the vast majority of CG sales, so solving problems in this relationship will be key to success.

CG leaders prioritize B2C relationships

CG companies have traditionally been separated from their end consumers, living primarily in the B2B realm and selling to retail and other indirect channel partners.

But with the continued adoption of ecommerce, CG brands can increasingly sell directly to — and build relationships with — their end consumer. Given this golden opportunity, CG leaders are overwhelmingly focused on going D2C. In our study, a full 99% of CG leaders say they are investing in D2C sales. Only 1% said this is not a priority.

Smart CG brands have both feet firmly planted in this direction. Adidas plans to double its online sales by 2020, and Burt’s Bees began piloting an ecommerce site in 2018. Its site includes compelling digital-only experiences that traditional retailers don’t offer, like limited-time sample boxes and lip shade finders.

Consumer goods leaders are evolving for the 2020s

CG leaders plan to adjust their financial investments to improve both B2B and B2C operations in the future. The two biggest areas of planned investment over the next three years are first-party consumer data and digital customer service support (82% plan to increase their investments in these).

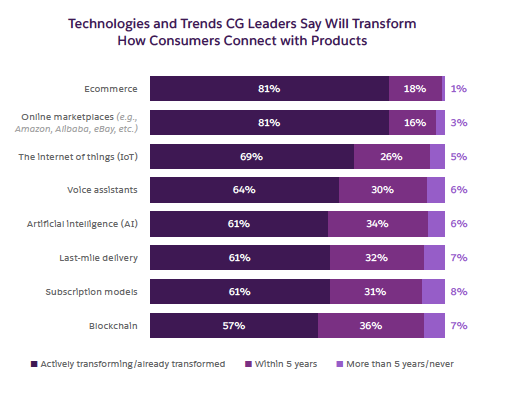

Within five years, 34% say AI will emerge as a key transformer in connecting shoppers with products, and 22% say it will do that in just two years.

Our data is tracking a massive shift in the consumer goods industry. For more insight into the priorities and challenges of 500 global industry leaders, download the new report: Consumer Goods and the Battle for B2B and B2C Relationships.