How to Calculate Recurring Revenue

It used to be that if a startup managed to raise $1 million from investors, it was considered a success.

Then came the rise of the so-called unicorn club, made up of private organizations that reached a valuation of more than $1 billion before going public.

Now, there’s even a live index of more than 400 startup unicorns around the world and variations honoring the businesses that have hit even larger valuation milestones. This includes the decacorn (valued at more than $10 billion) and the hectocorn (valued at more than $100 billion).

However, one of the biggest criticisms of private company valuations is that they’re inflated. Investors bet big on the company early on with the hope that it might get acquired or go public and be worth even more.

But for those who would rather rely on actual sales to determine a business’ value, a new category has emerged: the $100 million ARR club, with ARR being short for annual recurring revenue.

What is recurring revenue?

According to Investopedia, recurring revenue is “the portion of a company's revenue that is expected to continue in the future. Unlike one-off sales, these revenues are predictable, stable and can be counted on to occur at regular intervals going forward with a relatively high degree of certainty." Two important financial metrics are annual recurring revenue, or ARR, and monthly recurring revenue, abbreviated as MRR. TechTarget notes that when a company can reliably anticipate specific income every 30 days, that income is known as MRR.

Recurring revenue is every company’s goal.

Recurring revenue, at its most basic, can mean repeated, nonsubscription purchases from customers. For example, a car dealership may not rely on recurring revenue, but a company that sells essentials, such as disposable contact lenses or toilet paper, can generally count on multiple purchases from a customer.

Now, thanks to cloud computing, a number of software companies have been able to shift into a business model that relies on recurring revenue. In exchange for a monthly subscription payment, users can use powerful software that’s regularly updated, from photo-editing apps to CRM platforms. Some companies have subscription-based pricing for entertainment, as is the case with Netflix, or for household supplies, which Amazon offers with its Subscribe & Save feature.

Subscription-based business models have become the new goal.

In earlier business models, companies would sign customers up for large, multiyear contracts with payments delivered partially up front and split into project or service milestones. In other instances, engagements were short term and had no renewal period. This often meant that after a few months, the customer turned over. While these business models are still in use, they create unpredictable revenue streams or require specialized accounting methods.

To take advantage of the potential for MRR and a more predictable ARR, many organizations are increasingly using recurring revenue business models. Part of this motivation comes from wanting to build a longer-term and more sustainable company that’s not overly reliant on outside investors and speculative bets. Recurring revenue becomes the most prized success metric.

With a recurring revenue model, revenues become more predictable and companies are able to better plan ahead. Customers are also able to adjust their subscriptions as their needs change, allowing them to more easily manage their budgets and cash flow. Since they don’t have to pay large lump sums, they can budget more effectively and, when necessary, reevaluate their subscription expenses every 30 days.

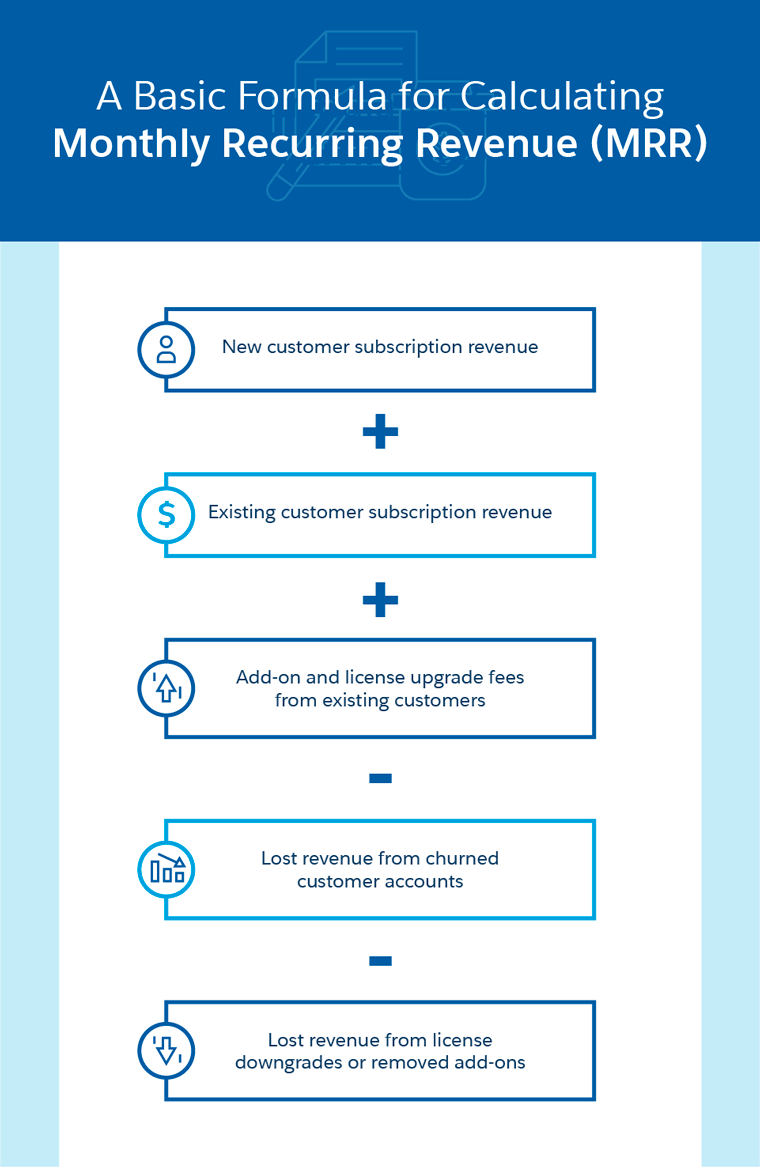

Here’s the formula to calculate monthly recurring revenue (MRR).

As more organizations adopt subscription sales models, it’s important to understand how to calculate recurring revenue. The easiest way to determine monthly recurring revenue is with the following formula:

New customer subscription revenue

+

Existing customer subscription revenue

+

Add-on and license upgrade fees from existing customers

-

Lost revenue from churned customer accounts

-

Lost revenue from license downgrades or removed add-ons

New versus existing customer subscription revenue: It’s important to distinguish between new and existing monthly subscriptions. This allows your business to evaluate the average duration of customer accounts separately from an upcoming anticipated turnover. Otherwise, you might assume that all customers from one month will fully carry over into the next, and for an indefinite period of time. By operating that way, you don’t take into account client churn.

Add-on and license upgrade fees: When appropriate, your account managers and product marketing specialists should encourage customers to upgrade their licenses and add on premium paid features.

Lost revenue: Naturally, customers come and go. Some might end their subscription, while others downgrade to a free or less expensive plan. In any case, business owners and sales managers have to account for all of these variables when calculating monthly recurring revenue.

Be aware that in most subscription-based businesses, customer acquisition and churn happen consistently throughout the year. However, that’s not always the case. Pay attention to potential seasonal fluctuations when making your calculations. For example, if your company provides bottled water to offices, average order sizes may increase during the hotter months of the year.

Here’s how to calculate annual recurring revenue (ARR).

You’ve already done the hard part. Once you’ve calculated MRR, multiply your monthly recurring revenue by 12 (for the 12 months of the year) to get your annual recurring revenue.

Know when to use MRR and ARR.

MRR is a metric that most teams should closely monitor each month. It gives you an immediate look at how well your sales team and marketing efforts are performing, whether or not your business is effective at customer retention, and if any recent product launches, updates, or pricing changes impacted customers.

Generally, companies look forward to month-over-month increases in MRR to compound their growth and progressively scale their business and operations. To do so, companies focus on nurturing loyalty among customers to minimize churn and increase average client billings. Customer acquisition is an important factor, too, but retention is a higher priority since high turnover can quickly undermine even the most successful acquisition campaigns.

For long-term planning, most companies look at ARR to help them project cash flow, determine upcoming budgets and investment decisions, and build their roadmap. This gives them a baseline expectation of how much revenue they’ll generate over the next 12 months. However, it’s more important that they consistently improve MRR in order to outperform any earlier annual revenue forecasts.

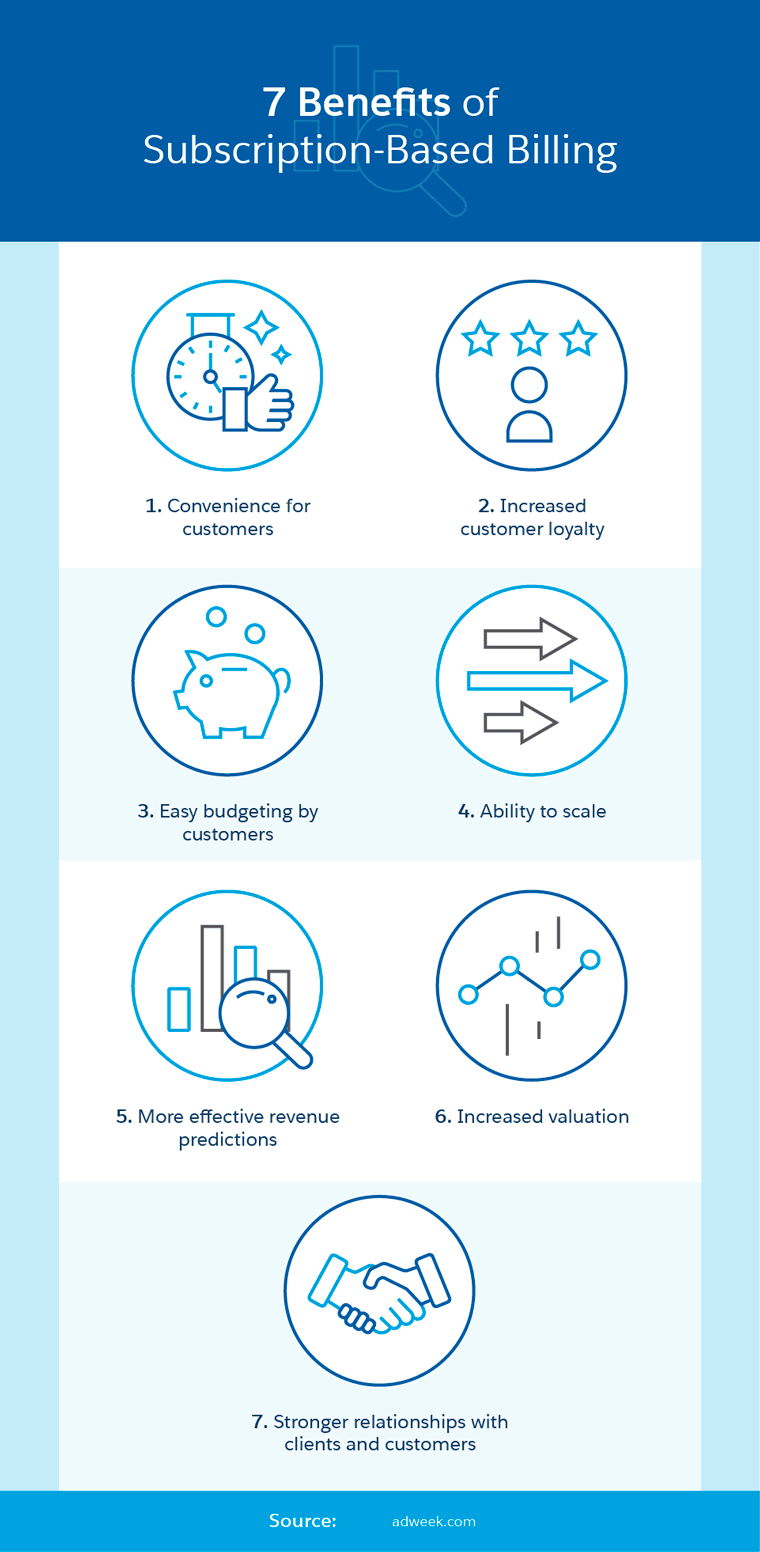

Subscription-based accounts impact companies and customers.

Subscription-based accounts make recurring revenue easy and predictable. At the same time, providers are accountable for delivering consistent value with their product or service, companies can access usage data to better innovate their solutions, and technology streamlines the onboarding process while also providing self-service upgrades.

Furthermore, subscription-based billing has created more accountability among sellers. Because most customers aren’t tied to long-term contracts with complicated termination clauses, businesses are expected to deliver consistent value and reliable service to their clients month after month.

Usage data becomes crucial to measure, too. For example, you need to monitor how much customers use your platform, which features they enjoy the most, and which they use the least in order to inform the company’s product development plans. Companies have worked hard to make it easier for prospects to quickly adopt their platforms, lowering the potential friction otherwise caused by switching costs.

Technology has also made it easier for buyers to sign up and start using a new subscription service. They can often seamlessly add on extra features each month or upgrade their subscription tier using a business’ self-service platform. This minimizes the need for account managers to frequently upsell users.

Consider these four strategies to improve recurring revenue.

Beyond simply calculating and monitoring MRR and ARR, companies can employ a few strategies to drive growth.

Offer Annual Licenses

To secure longer-term commitments, some companies offer discounts for an annual subscription, creating a win-win situation. Customers get to take advantage of the savings, and businesses maintain cash flow with a full year’s worth of fees up front. The annual commitment also helps minimize churn, since customers are less likely to end a subscription they’ve already paid for. One caveat: This method can complicate the way companies calculate monthly recurring revenue, but the gains in annual recurring revenue are often worth it.

Automate Payments

Earlier B2B sales processes required a lot of operational resources. Accounts receivable teams were required to know when and how often to bill clients after services were provided, what the contract terms were, and the names and contact information of all the important client-side contacts. Companies can save time by automatically withdrawing payments through linked bank accounts or credit cards on file at each successive monthly renewal date. Many CRMs facilitate this process, so you cut down on having to manually chase a delinquent invoice.

Send Delinquent Payment Notifications to End Users

Of course, if authorized payment methods fail, you can trigger in-app messages and automated emails that directly notify users to update their information. Previously, departments were more siloed, so if a customer’s finance department had a delay in responding to a payment inquiry, the company’s end users would still expect services to be rendered. Direct notifications incentivize end users to work with their internal teams to update their payment method or risk losing service.

Upgrade Your Accounting Tools

Accounting tools integrated with your CRM platform help businesses quickly determine MRR and ARR. This streamlines financial reporting and minimizes data errors because you can get a real-time update on the latest customer acquisition, retention, and average account size numbers.

Annual recurring revenue is a powerful indicator for success.

Annual recurring revenue is a powerful indicator for success. Many companies in the digital age have built their businesses on speculation. Absent real revenue, they rely on outside investors to finance their ambitions, and they place large, uncertain bets.

Other organizations have adopted a subscription-based model. Using this approach, they are able to build a more sustainable company, long term. By consistently delivering value to customers, they can confidently collect subscription payments that will fuel and finance further growth.

How to Calculate Recurring Revenue

It used to be that if a startup managed to raise $1 million from investors, it was considered a success.

Then came the rise of the so-called unicorn club, made up of private organizations that reached a valuation of more than $1 billion before going public.

Now, there’s even a live index of more than 400 startup unicorns around the world and variations honoring the businesses that have hit even larger valuation milestones. This includes the decacorn (valued at more than $10 billion) and the hectocorn (valued at more than $100 billion).

However, one of the biggest criticisms of private company valuations is that they’re inflated. Investors bet big on the company early on with the hope that it might get acquired or go public and be worth even more.

But for those who would rather rely on actual sales to determine a business’ value, a new category has emerged: the $100 million ARR club, with ARR being short for annual recurring revenue.

What is recurring revenue?

According to Investopedia, recurring revenue is “the portion of a company's revenue that is expected to continue in the future. Unlike one-off sales, these revenues are predictable, stable and can be counted on to occur at regular intervals going forward with a relatively high degree of certainty." Two important financial metrics are annual recurring revenue, or ARR, and monthly recurring revenue, abbreviated as MRR. TechTarget notes that when a company can reliably anticipate specific income every 30 days, that income is known as MRR.

Recurring revenue is every company’s goal.

Recurring revenue, at its most basic, can mean repeated, nonsubscription purchases from customers. For example, a car dealership may not rely on recurring revenue, but a company that sells essentials, such as disposable contact lenses or toilet paper, can generally count on multiple purchases from a customer.

Now, thanks to cloud computing, a number of software companies have been able to shift into a business model that relies on recurring revenue. In exchange for a monthly subscription payment, users can use powerful software that’s regularly updated, from photo-editing apps to CRM platforms. Some companies have subscription-based pricing for entertainment, as is the case with Netflix, or for household supplies, which Amazon offers with its Subscribe & Save feature.

Subscription-based business models have become the new goal.

In earlier business models, companies would sign customers up for large, multiyear contracts with payments delivered partially up front and split into project or service milestones. In other instances, engagements were short term and had no renewal period. This often meant that after a few months, the customer turned over. While these business models are still in use, they create unpredictable revenue streams or require specialized accounting methods.

To take advantage of the potential for MRR and a more predictable ARR, many organizations are increasingly using recurring revenue business models. Part of this motivation comes from wanting to build a longer-term and more sustainable company that’s not overly reliant on outside investors and speculative bets. Recurring revenue becomes the most prized success metric.

With a recurring revenue model, revenues become more predictable and companies are able to better plan ahead. Customers are also able to adjust their subscriptions as their needs change, allowing them to more easily manage their budgets and cash flow. Since they don’t have to pay large lump sums, they can budget more effectively and, when necessary, reevaluate their subscription expenses every 30 days.

Here’s the formula to calculate monthly recurring revenue (MRR).

As more organizations adopt subscription sales models, it’s important to understand how to calculate recurring revenue. The easiest way to determine monthly recurring revenue is with the following formula:

New customer subscription revenue

+

Existing customer subscription revenue

+

Add-on and license upgrade fees from existing customers

-

Lost revenue from churned customer accounts

-

Lost revenue from license downgrades or removed add-ons

New versus existing customer subscription revenue: It’s important to distinguish between new and existing monthly subscriptions. This allows your business to evaluate the average duration of customer accounts separately from an upcoming anticipated turnover. Otherwise, you might assume that all customers from one month will fully carry over into the next, and for an indefinite period of time. By operating that way, you don’t take into account client churn.

Add-on and license upgrade fees: When appropriate, your account managers and product marketing specialists should encourage customers to upgrade their licenses and add on premium paid features.

Lost revenue: Naturally, customers come and go. Some might end their subscription, while others downgrade to a free or less expensive plan. In any case, business owners and sales managers have to account for all of these variables when calculating monthly recurring revenue.

Be aware that in most subscription-based businesses, customer acquisition and churn happen consistently throughout the year. However, that’s not always the case. Pay attention to potential seasonal fluctuations when making your calculations. For example, if your company provides bottled water to offices, average order sizes may increase during the hotter months of the year.

Here’s how to calculate annual recurring revenue (ARR).

You’ve already done the hard part. Once you’ve calculated MRR, multiply your monthly recurring revenue by 12 (for the 12 months of the year) to get your annual recurring revenue.

Know when to use MRR and ARR.

MRR is a metric that most teams should closely monitor each month. It gives you an immediate look at how well your sales team and marketing efforts are performing, whether or not your business is effective at customer retention, and if any recent product launches, updates, or pricing changes impacted customers.

Generally, companies look forward to month-over-month increases in MRR to compound their growth and progressively scale their business and operations. To do so, companies focus on nurturing loyalty among customers to minimize churn and increase average client billings. Customer acquisition is an important factor, too, but retention is a higher priority since high turnover can quickly undermine even the most successful acquisition campaigns.

For long-term planning, most companies look at ARR to help them project cash flow, determine upcoming budgets and investment decisions, and build their roadmap. This gives them a baseline expectation of how much revenue they’ll generate over the next 12 months. However, it’s more important that they consistently improve MRR in order to outperform any earlier annual revenue forecasts.

Subscription-based accounts impact companies and customers.

Subscription-based accounts make recurring revenue easy and predictable. At the same time, providers are accountable for delivering consistent value with their product or service, companies can access usage data to better innovate their solutions, and technology streamlines the onboarding process while also providing self-service upgrades.

Furthermore, subscription-based billing has created more accountability among sellers. Because most customers aren’t tied to long-term contracts with complicated termination clauses, businesses are expected to deliver consistent value and reliable service to their clients month after month.

Usage data becomes crucial to measure, too. For example, you need to monitor how much customers use your platform, which features they enjoy the most, and which they use the least in order to inform the company’s product development plans. Companies have worked hard to make it easier for prospects to quickly adopt their platforms, lowering the potential friction otherwise caused by switching costs.

Technology has also made it easier for buyers to sign up and start using a new subscription service. They can often seamlessly add on extra features each month or upgrade their subscription tier using a business’ self-service platform. This minimizes the need for account managers to frequently upsell users.

Consider these four strategies to improve recurring revenue.

Beyond simply calculating and monitoring MRR and ARR, companies can employ a few strategies to drive growth.

Offer Annual Licenses

To secure longer-term commitments, some companies offer discounts for an annual subscription, creating a win-win situation. Customers get to take advantage of the savings, and businesses maintain cash flow with a full year’s worth of fees up front. The annual commitment also helps minimize churn, since customers are less likely to end a subscription they’ve already paid for. One caveat: This method can complicate the way companies calculate monthly recurring revenue, but the gains in annual recurring revenue are often worth it.

Automate Payments

Earlier B2B sales processes required a lot of operational resources. Accounts receivable teams were required to know when and how often to bill clients after services were provided, what the contract terms were, and the names and contact information of all the important client-side contacts. Companies can save time by automatically withdrawing payments through linked bank accounts or credit cards on file at each successive monthly renewal date. Many CRMs facilitate this process, so you cut down on having to manually chase a delinquent invoice.

Send Delinquent Payment Notifications to End Users

Of course, if authorized payment methods fail, you can trigger in-app messages and automated emails that directly notify users to update their information. Previously, departments were more siloed, so if a customer’s finance department had a delay in responding to a payment inquiry, the company’s end users would still expect services to be rendered. Direct notifications incentivize end users to work with their internal teams to update their payment method or risk losing service.

Upgrade Your Accounting Tools

Accounting tools integrated with your CRM platform help businesses quickly determine MRR and ARR. This streamlines financial reporting and minimizes data errors because you can get a real-time update on the latest customer acquisition, retention, and average account size numbers.

Annual recurring revenue is a powerful indicator for success.

Annual recurring revenue is a powerful indicator for success. Many companies in the digital age have built their businesses on speculation. Absent real revenue, they rely on outside investors to finance their ambitions, and they place large, uncertain bets.

Other organizations have adopted a subscription-based model. Using this approach, they are able to build a more sustainable company, long term. By consistently delivering value to customers, they can confidently collect subscription payments that will fuel and finance further growth.

About the Author

Jessica Bergmann

Senior Director of Content Marketing, Salesforce

Senior Director of Content Marketing, Salesforce

Jessica Bergmann is Senior Director of Content Marketing at Salesforce. She aligns with the broader organization to develop and execute global content and social media strategy including product, partner and digital marketing, customer success and retail practice. Prior to Salesforce, Jessica led global content development for brands like Dove, adidas, HEAD, Porsche and Rolex.

Share "How to Calculate Recurring Revenue" on your site:

<strong>Click To Enlarge</strong><br /><br />

<a href="https://www.salesforce.com/resources/articles/how-to-calculate-recurring-revenue" target="_blank">

<img src="https://www.salesforce.com/content/dam/web/en_us/www/images/resource-center/how-to-calculate-recurring-revenue-embed.jpg" alt="How to Calculate Recurring Revenue" width="600px" border="0" />

</a>

</p>

<p>Via <a href="https://www.salesforce.com/resources/articles/how-to-calculate-recurring-revenue" target="_blank">Salesforce</a> </p>

More sales resources to help you grow revenue faster.