Why Does Originating a Loan or Opening an Account in 2026 Still Feel Like 2006?

When "Yes" takes three weeks, your customer will seek out your competitors who operate faster.

Meet Jennifer. She’s applying for a small business loan to expand her coffee shop. Great credit score. Ten years of steady revenue. A banking relationship that predates her business itself.

She should be your dream customer.

Instead, she’s stuck in week two of a paper-chase nightmare—uploading the same tax return three times to different portals, waiting for callbacks from underwriters who can’t see she already has a mortgage and two credit cards with your bank, and watching her expansion opportunity slip away to a fintech that approved her in 48 hours.

This isn’t a customer experience problem. It’s revenue hemorrhage at scale.

Financial institutions lose $487 billion annually in abandoned origination journeys, according to McKinsey’s Digital Banking Report. The culprit? Fragmented legacy systems—what we call “Franken-tech”—stitched together over decades, where the lending department doesn’t talk to deposits, and nobody talks to the customer relationship platform. The result: 70% of financial institutions lost clients in the past year due to slow, inefficient onboarding — a record high, up from 67% in 2024 and 48% in 2023 (Fenergo Financial Crime Industry Trends, 2025), and 82%of contact center time is spent on operational and support tasks instead of customer needs and sales, a direct cost of disconnected systems and siloed data (Capgemini World Retail Banking Report, 2024).

When your origination process is held together by manual handoffs, document re-uploads, and systems that treat a 10-year customer like a stranger, you’re not competing for market share. You’re competing for survival.

Dismantling the Franken-Tech Era: Salesforce Launches Digital Origination

Salesforce Digital Origination is the industry’s first unified solution that replaces fragmented point solutions with a single, intelligent origination engine—one that works across every product line you offer. Not another siloed loan origination solution. Not another deposit account module. A complete rethink of how financial institutions bring customers into any journey: auto loans, commercial accounts, mortgages, treasury management, credit cards, deposit accounts.

This is the shift from Franken-tech to unified intelligence.

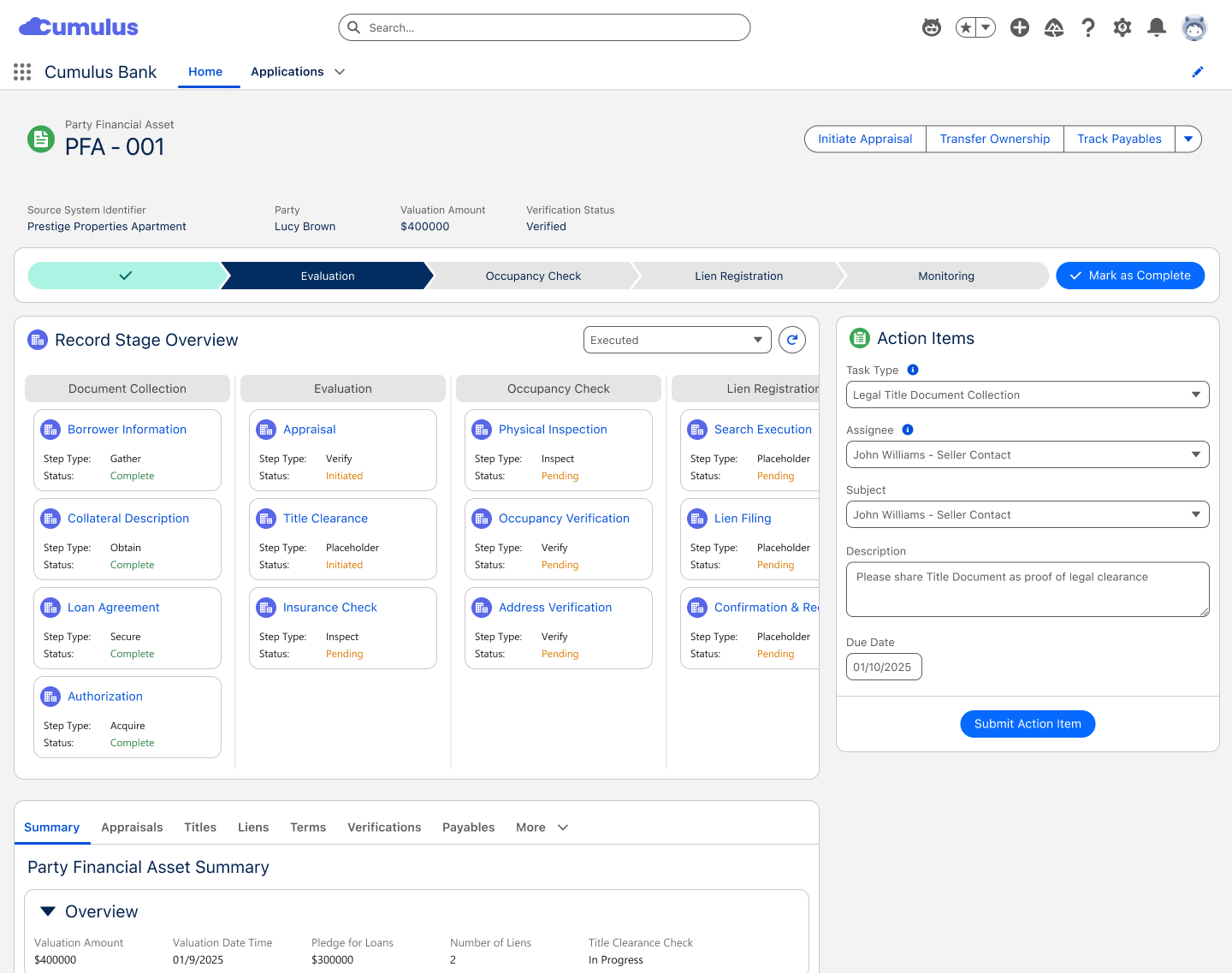

Built on Agentforce Financial Services and powered by Data Cloud, Digital Origination doesn’t just automate forms, it creates a Golden Thread of customer data that follows every applicant from first click to final approval.

The system your mortgage team uses? It already knows what your commercial banking team knows.

The underwriting console? It sees the full customer relationship, not just this application.

The AI document verification tool? It learns from every submission across every product line.

Here’s what that means in practice:

- Product catalogs customers can explore like they’re browsing streaming services, personalized recommendations based on their existing relationships

- Intelligent forms that adapt in real-time, never asking for information you already have

- AI-powered document extraction that reads tax returns, bank statements, and pay stubs in seconds, auto-populating fields and flagging discrepancies before humans waste time

- Underwriter consoles that present complete customer stories, not application fragments

- Approval workflows that route routine decisions to AI agents and escalate exceptions to experienced judgment

And because it integrates seamlessly with your existing core banking systems, credit bureaus, and verification providers, you’re not replacing your tech stack. You’re finally connecting it.

The question isn’t whether you can cut origination time by 70%. The question is whether you can afford not to while your competitors already have.

Salesforce Digital Origination

From loans to deposits, launch products faster and automate complex decisioning with a single, AI-powered solution built for speed and scale.

One Solution, Infinite Product Journeys: Built for Every Line of Business

Legacy thinking says you need different systems for different products. A loan origination system. A deposit account opening solution. A separate commercial onboarding process. Each with its own vendor, its own data model, its own training program, its own technical debt.

That model became a competitive liability.

Digital Origination provides pre-configured templates for every major product vertical—giving you 80% of what you need on day one, with the flexibility to customize the remaining 20% to your exact workflows. One solution. One data model. One truth about your customer.

Digital Origination for Lending handles the full spectrum of personal loans, auto financing, home equity, commercial real estate, asset-backed lending. Built-in credit decisioning, collateral management, and covenant tracking. Launch a new specialty lending program in weeks, not the 18-month build cycle your current vendor quoted.

Digital Origination for Deposit Accounts makes opening checking, savings, or money market accounts as frictionless as signing up for an app, but with KYC, BSA/AML, and beneficial ownership verification happening invisibly in the background. No compliance shortcuts. Just intelligent automation.

Digital Origination for Commercial Accounts navigates the complexity of multi-entity structures, cross-border treasury management, and business verification without burying relationship managers in paperwork. Your commercial team spends time building relationships, not chasing documents.

Digital Origination for Auto Loans & Leasing connects dealers, lenders, and buyers in real-time. Turn F&I offices into digital origination hubs where approvals happen before the test drive ends and funding happens before the customer leaves the lot.

And the possibilities extend across the entire product catalog: HELOC, student loans, credit cards, revolving lines of credit, alternate lending, B2B treasury services, collateral-backed loans, all managed from a single interface that learns and improves with every application.

One system. Every product. Zero silos.

Simplify Your Product Origination Journeys

Launch products faster by originating multiple journeys through a single, unified solution. Eliminate system toggling with an AI-powered solution that centralizes applicant summaries and offers built-in compliance.

How AI Makes Banking More Human

Let me show you what this looks like in the wild.

It’s 9:47 AM. Marcus, a loan officer at a regional credit union, gets a notification: Sarah Chen just started a HELOC application online. She’s been a member for 12 years. She has a mortgage, two car loans (both paid off), and a checking account with consistent direct deposits.

Marcus doesn’t know any of this yet, but Digital Origination already does.

He opens the application in his console. Instead of a blank form, he sees an AI-generated summary: “Long-term member. Excellent payment history. Current home value $485K based on recent Zestimate. Estimated equity $220K. Strong DTI at 24%. Flagged intent: likely home renovation based on recent contractor payments in transaction history. Recommended product: $75K HELOC, standard rate tier.“

The Loan Product Assistant—an AI agent trained on your product matrix and compliance rules, has already matched Sarah to the right offer. No product manual needed.

Marcus sends Sarah a text: “I see you’re exploring a home equity line. I can walk you through it when you’re ready.” Personal. Proactive. Humans.

Sarah responds: “Actually, I’m renovating the kitchen. Can I upload docs now?”

She uploads last three years tax documents, two W-2s, and six months of bank statements via her phone. Within 30 seconds, AI Document Verification has:

- Extracted income data and validated it against stated income

- Confirmed revenue with the submitted tax statement

- Flagged one tax statement as outdated and removed it from calculations

- Auto-populated every field in the income section

What used to take an analyst 45 minutes just happened faster than it takes Marcus to grab his second coffee.

Sarah’s application moves to underwriting. Maya, the underwriter, sees it in her Unified Underwriting Console. Not a form dump. Not a checklist. A complete customer story built by Data 360, the intelligence engine that connects every touchpoint Sarah’s ever had with the credit union.

She reviews the Collateral Management view: property lien position, recent revenue, no red flags. The Business Rules Engine has already pre-scored the application: Standard approval tier. No exceptions required.

Maya approves with two clicks. Sarah gets a congratulations email. Marcus gets a notification. Closing is scheduled for Thursday.

From application to approval: 4 hours. Not 4 weeks. Not 4 days. The same Tuesday.

But here’s what really matters: Sarah tells her sister about it at dinner. Her sister applies for a personal loan the next morning. That’s not just operational efficiency. That’s compounding competitive advantage.

Meanwhile, across town, a mortgage broker named James submits three loan applications through the credit union’s Financial Intermediary Center, the partner portal that lets him track his entire pipeline, upload borrower documents, and see real-time status updates without calling anyone. What used to require three phone calls and two emails now happens in two clicks. James closes his laptop and thinks: This is the easiest lender I work with. That’s not just operational efficiency. That’s how you win in an indirect channel business.]

Fundamentals of Digital Origination for Lending

Unlock efficiency in loan origination through digital transformation and innovative tools. Explore this trail to learn how to simplify the lending process from application to disbursement.

The Ecosystem Advantage Nobody Else Can Match

Every solution will promise you faster approvals. Most will claim “AI-powered automation.” A few will tout integrations.

None of them sit inside the Salesforce ecosystem. And that’s not marketing. That’s architecture.

Digital Origination is built on Agentforce Financial Services, which means it already understands the complexity of financial relationships including household structures, account hierarchies, referral networks, advisor assignments, beneficiaries. Digital Origination doesn’t just see this application. It sees this customer’s entire financial life with your institution.

It’s connected to Customer 360, giving you a complete view before the first form field is filled. You know this customer inquired about wealth management last quarter, opened a trust account for their daughter, and attended your financial planning seminar in March. That context doesn’t just improve underwriting. It transforms what’s possible in relationship banking.

Data Cloud, the intelligence engine behind the AI summaries, the document verification, the smart recommendations breaks down the data silos that make customers feel like strangers. When a loan closes, that customer’s journey data is immediately available to your relationship managers, your marketing automation, your retention teams, your analytics dashboards. No batch exports. No data lag. Real-time truth across every system.

And the AI capabilities powered by Agentforce don’t just automate repetitive tasks. They learn from your decisions, surface insights underwriters need, predict which applications need extra attention, generate summaries that save hours of review time, and flag fraud patterns that manual reviews miss.

This isn’t a feature list. It’s a fundamental structural advantage over every competitor still stuck stitching together point solutions.

Lower operational costs. Underwriters handle 3x the volume without quality loss. Loan officers spend time building relationships instead of chasing paperwork.

Faster time to value. Deploy new products in weeks using pre-built templates. Launch market tests without six-month implementation cycles. Reduced compliance risk. Audit trails built into every step. Business rules that enforce policy before approvals, not after violations. Customer satisfaction that drives organic growth. Net Promoter Scores that trend toward “actually delightful” instead of “painfully adequate.”

When your origination journey is connected to everything else you know about your customers, you’re not just processing applications faster. You’re building relationships that compound over decades.

From First Click to Lifelong Customer

Explore the innovative, AI-driven capabilities that turn routine account openings and loan applications into growth engines for your business.

The Competitive Necessity Test: What Happens When You Wait

Close your eyes for a moment. Imagine your best customer is the one whose household generates $12K in annual fees, refers two friends a year, and has been with you since they opened their first checking account in college.

Now imagine they apply for a new product tomorrow.

Do they feel like your best customer? Or do they feel like applicant #847 in a faceless queue? If the answer makes you wince, you have a competitive crisis that’s getting worse every quarter.

While you’re optimizing the old model, your competitors are replacing it entirely. And every month you wait, the gap widens.

Salesforce Digital Origination turns origination from necessary friction into your market differentiator. Turn approvals that used to take weeks into wins that happen the same day.

And because it’s built on a platform designed to evolve—with monthly releases, automatic Agentforce AI improvements, and an ecosystem of financial services innovation you’re not buying software that starts depreciating the moment it’s deployed. You’re investing in a solution that gets smarter with every application.

Faster decisions. Lower costs. Happier customers who tell their friends. And a system that adapts to regulation changes, fraud tactics, and customer expectations without custom development projects every time something shifts.

Your Move: The Choice That Defines the Next Decade

The financial services industry is splitting into two groups.

Institutions that treat origination as a cost center to optimize. And institutions that treat it as the first chapter of a lifetime relationship.

Which group will you be in five years?

Salesforce Digital Origination is available now, ready to transform how you bring customers into every product journey. The institutions deploying it today are cutting origination cycles by 70%, slashing operational costs by 40%, and seeing Net Promoter Scores climb into ranges they’ve never seen before.

The question isn’t whether origination needs to change.

The question is whether you’ll lead that change or be forced to follow it.

Understand how Digital Origination works in your environment. Experience it yourself.

AI supported the writers and editors who created this article.